Before You Believe the Doomers, Read These 7 Data Points on Housing Affordability

Portland Metro's housing market is shifting in ways the viral doom posts rarely capture. Here is what the actual data shows.

Before You Believe the Doomers, Read These 7 Data Points on Housing Affordability

Housing affordability has measurably improved since its 2022 peak. Monthly payments dropped in 2025, Portland buyers now have 4.3 months of inventory and real negotiating leverage, mortgage rates sit near 6%, and no credible economist is forecasting a crash. The full picture is more nuanced than social media suggests.

Housing is expensive. Rates are higher than they were in 2020. Prices went up. Rent has not been a bargain either. So when a scary chart pops up in your feed confirming all that frustration, it is easy to assume that is the whole story.

The good news? It is not. Affordability is not just about home prices. It is about mortgage rates, wage growth, inventory, negotiating power, and local supply. Over the past year, several of those pieces have started moving in a better direction. In my 20+ years working in sales and more than 10 years helping buyers and sellers across the Portland Metro area, I have seen markets cycle through fear and back into opportunity. This moment has the same shape.

So before you make a major financial decision based on a social media post, let's walk through what the data actually says and what it means for you here in Portland Metro. And if you want to see the historical context behind these numbers, you can dig into our full Portland market update archive going back to 1992.

Key Takeaways & Quick Navigation

- Mortgage Rates Have Eased and Refinancing Is Back on the Table

- The Buy vs. Rent Gap Is the Smallest It Has Been in Three Years

- Monthly Payments Actually Dropped in 2025

- Renters Are Getting Some Relief Too

- Builders Are Cutting Prices and Most Buyers Do Not Know It

- Buyers Finally Have More Room to Breathe

- No Serious Economist Is Forecasting a Housing Crash

- The Full Picture Is Bigger Than Any Viral Chart

- 5 Actions to Take Before Your Next Real Estate Decision

- Frequently Asked Questions

Where Things Stand Right Now

1. Mortgage Rates Have Eased and Refinancing Is Back on the Table

Rates drive your monthly payment more than almost anything else. As of mid-February 2026, the average 30-year fixed rate sits around 6.05%, according to Freddie Mac's Primary Mortgage Market Survey. Still above the 3% lows of early 2022, but meaningfully lower than when rates were pushing 7% and higher just over a year ago.

In early January, rate declines opened up refinance opportunities for nearly five million borrowers nationwide. For some families, that is the difference between feeling stretched and feeling stable. For others, it is the breathing room to start actually saving for a down payment. If you bought in the past two years and have not spoken to a lender recently, it may be worth a quick conversation about whether a refinance makes sense for your situation.

Running real numbers with a local lender changes the conversation. A 6% payment looks very different from what most people assumed when rates were at 7%.

Portland Buyer Math

The difference between a 6.8% rate and a 6.0% rate on Portland Metro's $510,000 median home is roughly $280 per month. That is a larger swing than most price negotiations produce. Rate movement is the story most buyers are not watching closely enough right now. You can explore current rate scenarios using Bankrate's mortgage calculator to see what these numbers look like for your specific purchase price.

Affordability recently hit its highest level in four years nationally. That does not mean homes are cheap, but the pressure has eased measurably from the peak. If you want historical context on Portland rate cycles going back to 1992, our Portland Metro market data page has the full picture in one place.

2. The Buy vs. Rent Gap Is the Smallest It Has Been in Three Years

For a while, buying felt so far out of reach that renters stopped running the numbers. Nationally, buyers need about $111,000 in annual income to afford a typical home. Renters need roughly $76,000 to afford a typical apartment, according to Zillow Research. That $35,000 income gap is still real, but it is the smallest it has been in three years, and it is narrowing.

Mortgage rates have dropped. Home price growth has slowed. Wages have continued to rise. None of that makes buying easy overnight, but the math is not as punishing as it was in 2022 when the gap was widening fast. In Portland Metro, HUD pegs the 2025 Area Median Family Income at $124,100, which puts a meaningful slice of working households within reach of today's payment math when combined with the right down payment strategy.

The Right Question to Ask

The question is not whether housing is expensive. It is. The better question is: does the difference between renting and owning still make sense for your situation right now? If your lease is up, run the actual side-by-side comparison with your real income, your down payment, and your Portland-specific plans. Our home evaluation page is a good starting point if you want to see what you could afford to buy.

3. Monthly Payments Actually Dropped in 2025

When people talk about affordability, what they are really asking is: what would my monthly payment be? Here is the part most doom posts missed. In 2025, homebuyer affordability improved 7.5% nationwide, per the National Association of Realtors. The median mortgage payment dropped to $2,025, down $102 per month from the year before.

Over twelve months, $102 per month is more than $1,200 per year. That is not a headline number, but it represents a real and measurable improvement in household purchasing power that never made it into the scary social media charts.

The Payment Numbers in Plain English

Portland Metro's $510,000 median home is more affordable on a monthly payment basis today than it was one year ago. The number that changed was not the price.

4. Renters Are Getting Some Relief Too

If you are renting right now, you have felt the squeeze of the past few years. Renewals kept coming in higher. Available units filled fast. Negotiating was not really an option. That pace has cooled.

Nationally, the typical household now spends 26.4% of income on rent, the lowest share since August 2021, per Zillow's Rental Market Report. The typical asking rent in January 2026 was $1,895, flat month over month and up just 2% from a year ago. That is the slowest annual rent growth since 2020. More units have come online, vacancy rates are up, and nearly 40% of rental listings are offering concessions like free first months or reduced deposits.

Portland Renter Action Item

If your lease is up in the next 90 days, do not automatically accept the renewal terms. Landlords have more competition now than at any point in the past three years. A direct conversation before you sign could save you hundreds per month, and that is money that could go toward a down payment instead. If you want to explore what first-time buyer programs might be available to you, reach out and let's walk through the options together.

5. Builders Are Cutting Prices and Most Buyers Do Not Know It

A lot of people assume new construction is always the expensive option. In early 2026, that assumption does not hold up. In Q4 2025, 19.3% of new homes had price cuts nationally, per John Burns Research and Consulting. That is actually slightly higher than the 18.3% of existing home sellers who reduced prices during the same period. Builders are out-discounting resale sellers right now.

Beyond straight price cuts, builders are offering mortgage rate buydowns and closing cost credits that resale sellers typically cannot match. A rate buydown can lower your effective mortgage rate by a full point or more, changing your monthly payment far more dramatically than a modest price reduction would. NerdWallet has a solid breakdown of how buydowns work if you want to understand the math before walking into a builder's sales office.

New construction in the Portland area is offering rate buydowns and closing cost incentives that resale sellers rarely can match. The deals are not on the sign out front. You have to ask.

The Part Most Buyers Miss

Portland area builders rarely advertise their best incentives publicly. You have to ask directly. If you have only been looking at resale homes, widening your search to include new construction could open up options at prices that genuinely surprise you. This is one of the clearest market advantages available right now that most buyers are not taking advantage of.

6. Buyers Finally Have More Room to Breathe

For the first time in years, Portland buyers are not competing with ten other offers on every house. Nationally, there are 37% more sellers than buyers right now, more than double the imbalance from one year ago, per Redfin Research. In Portland Metro specifically, January 2026 RMLS data shows 4.3 months of inventory, with homes averaging 89 days on market and 4,785 active listings against just 1,111 closings.

To put that in historical context: a balanced market in Portland has historically been around 3 to 4 months of supply. We are now clearly in buyer-friendly territory, something we have not seen consistently since before the pandemic.

With 89 average days on market and 4.3 months of inventory, Portland buyers today have time to think, compare, and negotiate. That is a real change from 2021 and 2022.

What This Buyer Leverage Looks Like in Practice

- Homes are sitting longer, giving you time to think instead of scramble

- Price reductions are more common, sometimes before you even make an offer

- Inspection contingencies, closing cost credits, and repair requests are back on the table

- You can walk away from a deal that does not feel right without losing your only option

- Comparing multiple properties side by side without pressure is possible again

If you stepped back from the market in 2021 or 2022 because it felt chaotic, the environment today is genuinely different. The key is knowing which specific Portland neighborhoods still lean toward sellers and which have clearly shifted. Not all areas are moving at the same pace. Our neighborhood-level market updates break this down so you know exactly where you stand before making an offer.

7. No Serious Economist Is Forecasting a Housing Crash

A lot of people are still waiting for "the crash." You see it in the comments on every real estate post. "Just wait." "It's all coming down." "This is 2008 all over again." The problem with that narrative is that the people who actually study housing markets for a living are not saying that.

Home price forecasts for 2026 range from a slight dip of -0.3% to modest growth of +4.3%, according to compiled forecasts from CoreLogic and Fannie Mae's Housing Forecast. That is not a boom. It is not a collapse. Every major forecast also projects home sales volume to increase from the 4.06 million transactions recorded in 2025. Mortgage rate forecasts land between 6.0% and 6.5% as an annual average.

Why 2026 Is Not 2008

The 2008 crash required three converging forces that do not exist in today's market:

- Reckless lending standards. Today, underwriting is strict. Buyers must qualify. The Ability-to-Repay rule has fundamentally changed the risk profile of new mortgages.

- Forced mass selling. Unemployment is low. Most homeowners are not distressed.

- A supply flood. Inventory is building slowly from historically low levels, not flooding the market.

The Full Picture Is Bigger Than Any Viral Chart

Yes, prices went up. Yes, rates jumped. Yes, rents climbed. That part is entirely real. But what usually gets left out is what has happened since the peak. Rates have eased. Monthly payments came down in 2025. Rent growth has slowed. Builders are offering incentives most buyers do not know to ask about. In many parts of Portland, buyers finally have the time and leverage to make thoughtful decisions instead of panicked ones.

The only numbers that actually matter in your decision are yours. Your income. Your timeline. Your goals here in Portland Metro. I have been tracking this market through every cycle since 2003, and I can tell you that the buyers who make the best decisions are the ones who look at their own data, not the Twitter feed. That is a more productive conversation than any viral chart can start.

5 Actions to Take Before Your Next Real Estate Decision

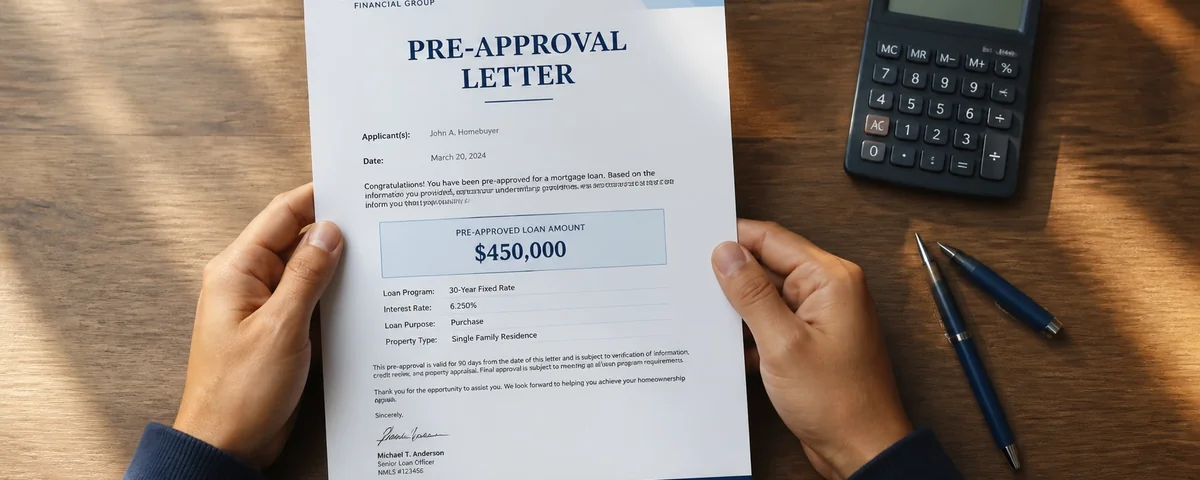

- Get a real pre-approval, not an estimate. Portland's median is $510,000 and rates are near 6%. Know your actual payment before you form an opinion about whether you can afford it. I can connect you with a local lender I trust if you need a starting point.

- Negotiate terms, not just price. With 4.3 months of inventory, buyers can ask for closing cost assistance, inspection contingencies, and appraisal protections. Use that leverage. Our buyer's guide walks through exactly how to structure an offer in today's market.

- Ask about new construction incentives. Builders are offering rate buydowns and credits that resale sellers cannot match. Widen your search before writing it off.

- Talk to your landlord before auto-renewing. Vacancy rates are up and concessions are common. You have more leverage than you did two years ago.

- Think in five-year horizons, not headlines. If you have stable employment and a long-term plan, current conditions offer real opportunity. Investopedia breaks down the long-term case for homeownership if you want an objective third-party perspective.

Frequently Asked Questions

Click any question to read the answer.

Is 2026 a good time to buy a home in Portland?

What is the buy vs. rent income gap right now?

Are mortgage rates expected to drop further in 2026?

Why are there 37% more sellers than buyers right now?

Are builders really cutting prices on new homes in Portland?

Should I wait for Portland home prices to drop more before buying?

Is a housing crash coming in 2026?

Ready to Look at Your Real Numbers?

I work with Portland buyers and sellers every day. I can walk you through what current conditions mean for your specific situation, whether you are buying, thinking about selling, or just trying to figure out if now is the right time to make a move. When you are ready, I am here.

Categories

Recent Posts

GET MORE INFORMATION