Mortgage Pre-Approval in Oregon: A Portland Buyer's Guide

Northwest Portland, Oregon. A couple reviewing pre-approval documents at home before starting their search.

Getting pre-approved for a mortgage is the moment when buying a home stops being an idea and starts being a plan. In the Portland metro market, most listing agents will not even forward your offer without a pre-approval letter attached. This guide covers what pre-approval actually is, how Oregon's main loan types compare, and how to choose a lender who will still answer the phone on closing day.

How do I get pre-approved for a mortgage in Oregon?

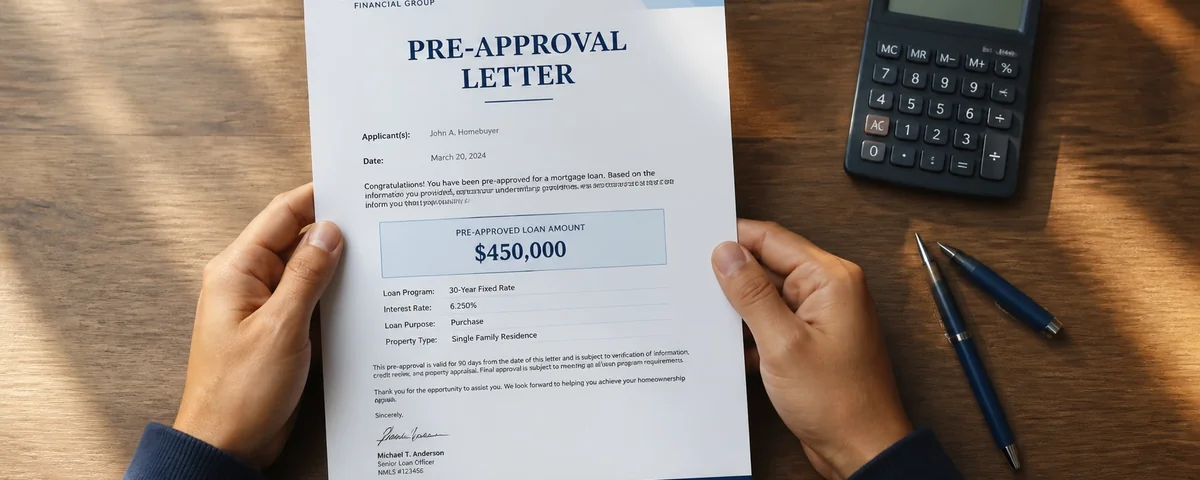

Getting pre-approved for a mortgage in Oregon takes one to three business days once you submit documents to a lender. You provide pay stubs, W-2s or tax returns, bank statements, ID, and a list of debts. The lender pulls your credit, verifies your income and assets, and issues a pre-approval letter showing the loan amount, estimated rate, and loan type you qualify for. Most pre-approval letters are valid for 60 to 90 days. In the Portland metro market, sellers routinely refuse offers without one, so this is your starting line, not a later step.

→ Bottom line: plan on roughly two weeks from "I want to buy" to "I am pre-approved and offer-ready" if your documents are organized.

- Pre-Qualification vs Pre-Approval: Why the Difference Matters

- The Three C's: How Lenders Decide What You Can Borrow

- Loan Types in Oregon: Which One Fits Your Situation

- Rate Lock: When to Lock and Why Timing Matters

- Underwriting: How to Protect Your Approval

- Down Payment Assistance Programs in Oregon

- How to Choose a Portland Mortgage Lender

- The Loan Estimate: How to Compare Lenders

- When This Does Not Apply

- Frequently Asked Questions

Pre-Qualification vs Pre-Approval: Why the Difference Matters

These two terms get used interchangeably in casual conversation, but they are not the same thing. A pre-qualification is a quick estimate based on what you tell a lender about yourself. A pre-approval is a verified analysis based on documents the lender has actually reviewed. In a competitive Portland offer situation, that distinction shows up the moment the listing agent reads your offer.

Pre-qualification can happen in fifteen minutes online with no documentation. It tells you what you might qualify for. Pre-approval requires the lender to pull your credit, verify your income, verify your assets, and review your debts. It tells you what you actually qualify for and produces a letter you can attach to an offer.

What sellers actually see when reading your offer

A pre-qualification letter from a national online lender and a fully underwritten pre-approval from a local Portland lender do not carry the same weight. Many listing agents in this market discount or skip offers backed only by pre-qualification because the financing risk is materially higher. Ask your lender for a fully underwritten pre-approval when possible. It means your file has been reviewed by an underwriter, not just an automated system.

Source: Oregon mortgage broker reporting, 2026.

The Three C's: How Lenders Decide What You Can Borrow

Lenders evaluate three factors when deciding whether to approve a loan and at what amount. These are sometimes called the Three C's: Credit, Capacity, and Collateral. Understanding each one makes the entire process less mysterious and helps you spot what to work on before you apply.

Credit

Your credit score and credit history tell the lender how reliably you pay back what you borrow. Different loan types have different minimum scores, but in general a score of 740 or higher gets you the best rates. The 620 to 680 range still qualifies for most loans but at slightly higher rates. Below 620 your options narrow, though FHA loans can go lower with compensating factors.

Before you apply, pull your own credit through AnnualCreditReport.com, the federally mandated free credit report site. You get one free pull per bureau per year. Look for errors first, especially old accounts marked open that should be closed, or late payments that were not actually late. Disputes take 30 to 45 days to resolve, so do this early.

Capacity

Capacity is your debt-to-income ratio, or DTI. This is the percentage of your gross monthly income that goes to debt payments including your future mortgage. Most lenders want a DTI of 43 percent or lower, with the strongest files at 36 percent or lower. If you make $8,000 per month and your debts plus your future mortgage payment total $3,000, your DTI is 37.5 percent.

The lender looks at two DTI numbers. The front-end ratio is your housing cost alone. The back-end ratio includes housing plus all other debts. Both matter. If your DTI is borderline, paying down a credit card or two before applying can move you into a lower-rate tier.

Collateral

Collateral is the home itself. The lender wants to make sure the property is worth at least what you are borrowing against it, which is why an appraisal is part of every purchase loan. For pre-approval, collateral mostly shows up as the loan-to-value ratio, or LTV. If you put 10 percent down, your LTV is 90 percent. The lower the LTV, the lower the lender's risk and often the better your rate.

Loan Types in Oregon: Which One Fits Your Situation

Most Portland metro buyers will choose between four loan types. Each one is designed for a different situation. The right choice depends on your down payment, credit score, military status, and the price point of the home you are buying. Tap a loan type below to see how it works.

FHA Loan

Backed by the Federal Housing Administration. Designed for buyers with lower down payments or lower credit scores.

FHA loans are owner-occupied only and the home must meet FHA property standards, which can be stricter than conventional appraisals.

VA Loan

Backed by the Department of Veterans Affairs. Available to eligible active duty, veterans, and qualifying surviving spouses.

VA loans are owner-occupied only. Confirm your Certificate of Eligibility with the VA before applying. Visit VA Home Loans for eligibility details.

Conventional Loan

The most common loan type. Not backed by a government agency, but typically eligible for purchase by Fannie Mae or Freddie Mac.

Conventional loans can be used for primary residences, second homes, and investment properties, though terms vary by occupancy.

Jumbo Loan

For loan amounts above the conforming limit. Required for higher-priced Portland metro purchases.

Jumbo loans require more rigorous qualification — stronger credit, lower DTI, and often six months or more of reserves in the bank after closing.

Not sure you are ready to buy yet? Start by figuring out what monthly payment fits your life. The how much house you can afford in Portland guide walks through the math before you talk to a lender.

Rate Lock: When to Lock and Why Timing Matters

Mortgage rates move daily. A rate lock is an agreement with your lender that the rate quoted today will be the rate you get at closing, even if market rates rise in between. Most locks last 30, 45, or 60 days. Longer locks are available but cost more.

You cannot lock a rate before you have an accepted offer in most cases, because the lender needs the property address and contract details. Once you have an accepted offer, the question becomes whether to lock immediately or float for a few days hoping for a better number. For most buyers in most markets, locking immediately is the safer choice. The downside risk of rates moving up is usually larger than the upside of rates moving down by closing.

Letting your rate lock expire is expensive

If your lock expires before closing, you either pay an extension fee or you get whatever the current market rate is. In a rising-rate environment, that can mean hundreds of dollars per month for the life of the loan. If your file is moving slowly, ask about a lock extension well before the expiration date — not the day before.

Rate context matters too. As of April 2026, the average 30-year fixed rate sat near 6.46 percent according to Freddie Mac's weekly survey. That figure moves week to week, but it gives you a baseline to compare your quoted rate against. If you want to dig into rate strategy beyond pre-approval, see lower your mortgage rate.

Underwriting: How to Protect Your Approval

Underwriting is the period between your accepted offer and your closing day when the lender does a final, detailed review of your file. Underwriters re-pull your credit, re-verify your employment, and look for anything that changed since pre-approval. This is the most common point where deals fall apart, and almost always for reasons buyers did not realize would matter.

What to avoid between pre-approval and closing

Do not change jobs unless you have to. Do not open new credit cards. Do not finance a car, a couch, or anything else. Do not make large unexplained deposits into your bank account. Do not co-sign a loan for anyone. Do not let your credit utilization spike. The rule of thumb: between offer and closing, your financial life should look exactly like it did the day you got pre-approved.

If something does change — a job offer, an inheritance, a large gift — tell your lender immediately. They can usually work around it if they know about it in advance. They cannot work around it if they find out from a final credit pull two days before closing.

Down Payment Assistance Programs in Oregon

Oregon has one of the more robust down payment assistance program stacks in the country, administered primarily through Oregon Housing and Community Services. These programs are not a quick form on a website — they require a HUD-approved homebuyer education course, income verification, and coordination with an OHCS-approved lender. But for buyers who qualify, the assistance can be meaningful.

The Oregon Bond Residential Loan Program offers two options: Cash Advantage (below-market rate plus 3 percent of the loan amount toward closing costs) and Rate Advantage (a lower below-market rate with no cash assistance). The Flex Lending program through OHCS layers a second loan of 4 to 5 percent of the first mortgage to cover down payment and closing costs.

As of January 2026, OHCS's Down Payment Assistance Program offers eligible first-time and first-generation buyers up to $60,000 or 20 percent of purchase price, whichever is less, with 25 percent of funds reserved for Oregon veterans. Eligibility includes income limits, credit score minimums (typically 640), and completion of a homebuyer education course before applying. Oregon also offers a First-Time Home Buyer Savings Account allowing up to $6,125 annually deducted from Oregon taxable income through December 31, 2026.

If you are a first-time buyer in Oregon, the right move is to ask your lender directly whether you qualify for OHCS programs and which ones make sense for your situation. A lender who is not proactively surfacing these options on your behalf is a red flag. For broader context on the first-time buyer journey, see the first-time home buyer guide for Portland.

How to Choose a Portland Mortgage Lender

Choosing a lender matters more than most buyers realize. The rate is part of it, but the larger factor is communication. A lender who answers the phone, returns calls inside the day, and proactively flags issues before they become problems will save you money and stress. A lender who goes quiet under pressure will cost you both, sometimes the deal itself.

Get pre-approved with at least two lenders before committing to one. The pre-approval process costs nothing in fees, and a hard credit pull from multiple mortgage lenders within a 14 to 45 day window counts as a single inquiry on your FICO score. Use the comparison to evaluate not just the rate but the experience. Did they respond quickly? Did they explain things clearly? Did they ask thoughtful questions about your situation? Those signals predict how the rest of the loan will go.

Questions worth asking every lender you interview:

- What is your typical turnaround time from contract to clear-to-close?

- Do you originate loans locally or pass them off to a remote underwriting team?

- Are you offering a fully underwritten pre-approval or just an automated approval?

- What programs am I eligible for that I might not know about? (Listen for OHCS, VA, first-time buyer credits)

- How do you handle communication if something comes up after-hours or on a weekend?

- Can I see a sample Loan Estimate based on the home price range I am targeting?

In my last twelve Portland metro closings, the deals that closed on time without surprises all had one thing in common: a lender who returned calls inside the hour. The ones that stalled had a lender who went quiet under pressure. That pattern is so consistent I would rather work with a responsive lender at a slightly higher rate than the cheapest one who vanishes during underwriting.

Field note

The Loan Estimate: How to Compare Lenders

The Loan Estimate is a three-page standardized document the lender must give you within three business days of receiving your loan application. It exists specifically so you can compare offers from different lenders without trying to decode their internal terminology. Every Loan Estimate has the same sections in the same order, which makes apples-to-apples comparison possible.

The three sections worth focusing on first:

- Loan Terms — interest rate, monthly principal and interest, whether the rate or payment can increase, and whether there is a prepayment penalty or balloon payment.

- Projected Payments — your total monthly payment including taxes and insurance, and how that payment may change over time.

- Costs at Closing — total estimated closing costs and total estimated cash to close. This is where lender fee differences become visible.

When comparing two Loan Estimates, the rate is only one variable. Lender origination fees, points, and discount fees can shift the total cost meaningfully even when rates look similar. The CFPB's Loan Estimate explainer walks through every line of the document with a sample form.

The Loan Estimate also gives you your first realistic look at closing costs. For most Portland buyers, closing costs run 2 to 5 percent of the purchase price. If that number is new to you, see closing costs in Oregon for a line-by-line breakdown.

When This Does Not Apply

Situations where standard pre-approval timelines and guidance shift

Self-employed buyers, recent job changers, buyers with active credit events (short sales, bankruptcies, foreclosures still on credit), and buyers using significant gift funds for down payment all face longer and more documentation-heavy pre-approval processes. Self-employed buyers typically need two years of tax returns plus year-to-date profit and loss. Job changers may need to wait until they have completed a probationary period. Gift funds require a signed gift letter and often a paper trail showing the funds in the donor's account. If any of these apply to you, start the pre-approval conversation earlier — not later — and pick a lender experienced in non-standard files.

Frequently Asked Questions

What is the difference between pre-qualification and pre-approval?

Pre-qualification is a quick estimate based on what you tell a lender about yourself, with no documentation verified. Pre-approval is a verified analysis based on documents the lender has actually reviewed, including a credit pull, income verification, and asset verification. Pre-qualification produces a rough number. Pre-approval produces a letter you can attach to an offer. In the Portland metro market, sellers and listing agents typically discount or skip offers backed only by pre-qualification.

How long does mortgage pre-approval take?

Pre-approval typically takes one to three business days once you submit all required documents. The timeline depends on how quickly you provide your pay stubs, W-2s or tax returns, bank statements, and ID, and on the lender's internal turnaround. Self-employed buyers and buyers with non-standard income usually take longer. A fully underwritten pre-approval, where an underwriter has actually reviewed your file rather than just an automated system, takes longer but carries more weight with sellers.

What credit score do I need to buy a house in Oregon?

The minimum varies by loan type. FHA loans can go as low as 580 with a 3.5 percent down payment, and as low as 500 with 10 percent down. VA loans have no VA-set minimum, but most lenders require 620 or higher. Conventional loans typically require 620 minimum, with 740 or higher getting the best rates. Jumbo loans usually require 700 or higher. If your score is below 620, talk to a lender about whether FHA or compensating factors can still get you approved.

How much does mortgage pre-approval cost?

Pre-approval is typically free. Reputable lenders do not charge for the pre-approval process itself, including the credit pull. You will pay for credit reports, appraisals, and other costs later in the process once you have an accepted offer, but the pre-approval phase should not cost you anything. If a lender is asking for upfront fees just to pre-approve you, that is a red flag.

Does getting pre-approved hurt my credit score?

A pre-approval requires a hard credit inquiry, which can temporarily lower your score by a few points. However, FICO models treat multiple mortgage inquiries within a 14 to 45 day window as a single inquiry for scoring purposes. This means you can shop with multiple lenders during that window without compounding the impact on your score. To minimize impact, do your lender shopping inside a two-week window.

How long is a pre-approval letter good for?

Most pre-approval letters are valid for 60 to 90 days. If you have not found a home in that window, your lender can refresh the letter by re-pulling credit and re-verifying recent pay stubs and bank statements. The refresh is usually quick. If your financial situation has changed significantly, the lender may need to redo more of the analysis before issuing a new letter.

Can I make an offer on a house without a pre-approval?

Technically yes, but in the Portland metro market most sellers will not accept an offer without proof of financing. Cash buyers can submit proof of funds instead. For financed buyers, an offer without a pre-approval letter signals that the financing risk is unknown, which makes the offer less attractive even at a higher price. The pre-approval is your starting line, not a later step.

What if my financial situation changes after pre-approval?

Tell your lender immediately. Job changes, large deposits, new debt, or any other material change can affect your final approval. Lenders can often work around these changes if they know in advance, but they cannot work around surprises discovered during the final credit pull two days before closing. Treat the pre-approval as a commitment to keep your financial life stable until closing.

Ready to start a conversation about your situation?

Pre-approval is one of the few steps where a small amount of preparation changes everything that comes after. If you want to talk through which loan type fits your situation, which Portland lenders I trust, or how the overall process looks from where you are standing right now, get in touch. No pressure, no agenda — just a real conversation about your goals.

Homes for Sale in the Portland Metro Area

Data Sources & Verification

Data verified: May 2026

The information in this post is for general educational purposes and does not constitute financial, legal, or tax advice. Loan limits, program eligibility, and interest rates change frequently. Consult a qualified lender, financial advisor, or tax professional for guidance specific to your situation.

Saling Homes at eXp Realty is committed to equal housing opportunity. We do not discriminate on the basis of race, color, religion, sex, handicap, familial status, or national origin.

Categories

Recent Posts

GET MORE INFORMATION