First-Time Home Buyer Guide Portland: Every Step From Pre-Approval to Keys

The front porch of a Craftsman home in Portland, Oregon. For many first-time buyers, this is the moment the search becomes real.

Buying your first home in Portland is exciting, stressful, and one of the biggest financial decisions you will make. The process involves more moving parts than most people expect, and the Portland metro market has its own quirks that national guides never cover. This post walks you through what to expect at each stage, what Portland-specific factors will affect your experience, and where the right guidance makes the biggest difference.

First-Time Buyers in Portland

Start with a lender conversation and a pre-approval letter before you look at a single home. Portland metro prices generally sit above $500,000, but entry points exist in the $350,000 to $450,000 range depending on where you look and what type of property you are open to. Oregon offers several down payment assistance programs that can reduce your upfront costs, and the current market gives buyers more negotiating room than they have had in years. The process from pre-approval to keys typically takes 45 to 60 days once you find the right home, and having a local agent who understands Portland's neighborhoods, pricing patterns, and negotiation dynamics can save you thousands of dollars and months of frustration.

- Get Your Financial Foundation in Order

- Why Pre-Approval Comes Before House Hunting

- Oregon Programs That Can Help With Upfront Costs

- What Your Budget Actually Gets You in Portland

- Why the Right Agent Changes Everything

- House Hunting in Portland: What to Expect

- From Offer to Keys: What Happens After You Find the One

- When This Guide Does Not Apply

- Why Buyers Work With Joe

- Frequently Asked Questions

Get Your Financial Foundation in Order

The biggest mistake first-time buyers make is browsing listings before understanding their financial picture. Before you open a single listing, you need to know three things: your credit score, your debt-to-income ratio, and how much cash you have available.

Your credit score determines which loan programs you qualify for and what interest rate you receive. In Oregon, most programs require a minimum score of 620, though some options work with lower scores. The difference between a 680 and a 740 can mean tens of thousands of dollars over the life of your loan.

Your debt-to-income ratio compares your monthly obligations to your gross income. Lenders generally want this below 43%, though some programs allow up to 50%. Car payments, student loans, credit card minimums, and your projected mortgage payment all count toward that number.

Then there is the cash picture. You will need money for a down payment (anywhere from 3% to 20% depending on your loan type), closing costs (typically 2% to 5% of the purchase price in Oregon), and a reserve fund so you are not stretched thin the day you move in. If your numbers need work, give yourself 3 to 6 months to strengthen your position before applying for pre-approval. That time is never wasted.

Build Your Financial Snapshot

Pull your credit report from all three bureaus at AnnualCreditReport.com. Calculate your DTI by dividing total monthly debt by gross monthly income. Add up your available savings. Bring these three numbers to your first lender conversation. This one step puts you ahead of most first-time buyers who start the process without a clear picture of where they stand.

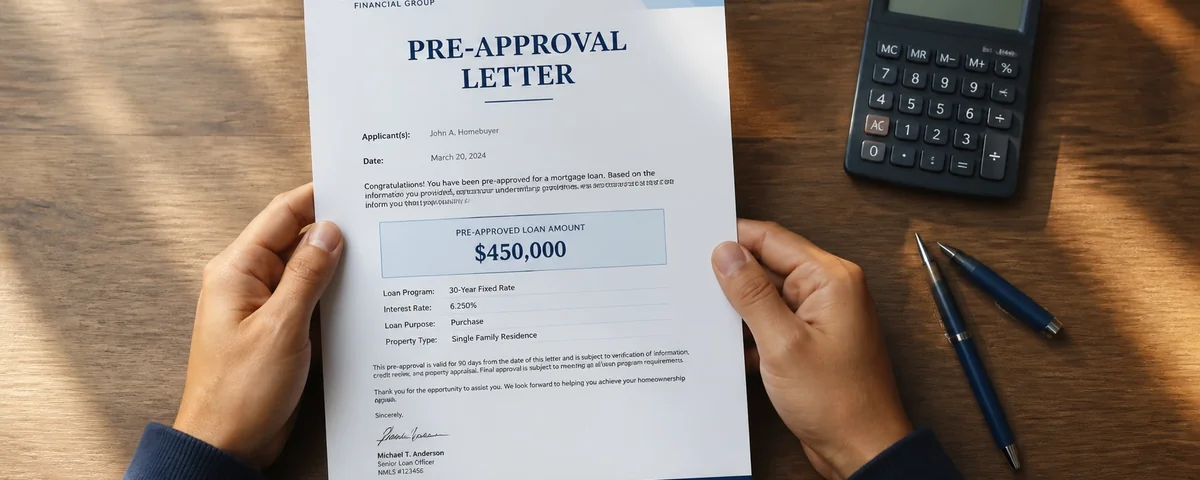

Why Pre-Approval Comes Before House Hunting

Pre-approval is not the same as pre-qualification. Pre-qualification is an estimate. Pre-approval means a lender has verified your income, pulled your credit, reviewed your assets, and issued a letter stating how much they will lend you. In Portland, sellers and listing agents take pre-approval letters seriously. Without one, your offer goes to the bottom of the pile.

The process typically takes one to three business days. Your lender will need two years of tax returns, recent pay stubs, bank statements, and identification. They will also walk you through which loan type fits your situation and what your realistic price range looks like.

One important point: your pre-approval amount is a ceiling, not a target. Just because a lender approves you for $550,000 does not mean you should spend that much. Build your budget around a comfortable monthly payment rather than the maximum a bank will approve. The costs that come with owning a home, including property taxes, insurance, maintenance, and the expenses beyond the mortgage payment, add up quickly. Your lender and your agent should both be helping you think about the full picture, not just the loan amount.

Oregon Programs That Can Help With Upfront Costs

Oregon and the Portland metro area offer several down payment assistance and closing cost programs for first-time buyers and buyers who meet certain income thresholds. These programs exist at the state level, the city level, and through local nonprofits. Some provide grants. Some provide forgivable loans. Some offer tax-advantaged savings tools. The details, eligibility requirements, and availability change regularly, which is why your lender should be the one walking you through what is current and what you qualify for.

Here is the important part: not every lender participates in every program. If your lender is not proactively bringing up assistance options during your pre-approval conversation, ask them directly what programs they offer for first-time buyers in Oregon. If they do not have good answers, that is worth paying attention to. A lender who specializes in first-time buyers in this market should know what is available and how to pair those programs with your mortgage. If yours does not, it may be worth talking to one who does.

Your Lender Should Be Leading This Conversation

Down payment and closing cost assistance can make the difference between being ready to buy now and waiting another year. But these programs have specific eligibility windows, funding limits, and education requirements. Your lender should be the one telling you what is available, not the other way around. If you are not hearing about assistance options during your pre-approval process, ask. And if the answers are vague, consider getting a second opinion from a lender who works with these programs regularly.

For more on strategies to secure a lower mortgage rate, including points, timing, and credit optimization, we cover that in a separate post.

What Your Budget Actually Gets You in Portland

Portland's median home price sits above $500,000 for the metro area, but that number does not tell the whole story. What you actually get depends heavily on where you look and what type of property you are open to.

In areas like outer Southeast Portland, Gresham, and parts of North Portland, entry points in the $350,000 to $450,000 range do exist. These might be older homes that need cosmetic updates, condos, or smaller bungalows, but they are real paths into ownership. Move into Beaverton, Tigard, or Milwaukie and the $450,000 to $550,000 range opens up more options with better commute access. Above $550,000, you are looking at larger homes in places like Lake Oswego, West Linn, and Portland's more established neighborhoods.

Here is the part that national guides miss: a $475,000 home in Beaverton and a $475,000 home in outer Gresham are completely different conversations. The neighborhoods, the appreciation patterns, the commute realities, and the resale profiles are not the same. This is where working with someone who knows the Portland market at the neighborhood level makes a real difference. The numbers on a listing tell you the price. They do not tell you whether that price represents a good investment for your specific situation.

For more on how Portland's pricing compares to what you might expect, take a look at the data points on Portland affordability.

Not Sure Where Your Budget Goes Furthest?

That is exactly the kind of question I help buyers answer every day. Every price point plays differently depending on the area, the property type, and your priorities. If you want to understand what your budget actually looks like in the neighborhoods you are considering, let's have that conversation. No pressure, just clarity.

Why the Right Agent Changes Everything

Buying a home is a process with a lot of professionals involved: your lender, your inspector, the title company, the listing agent on the other side. Your agent is the one person whose job is to look out for your interests across all of those interactions.

For first-time buyers, a good agent does more than open doors and write offers. They help you understand what you are looking at. They know which Portland neighborhoods have underground oil tank risk from the mid-1900s. They know which areas are seeing price adjustments and which ones are holding firm. They know when a listing has been sitting because of a pricing problem versus a structural problem. They know how to read an inspection report and which items are negotiation leverage versus normal wear and tear.

In Portland specifically, the market varies so much from one area to another that general advice breaks down fast. The dynamics in Lake Oswego are nothing like the dynamics in Milwaukie, even though they are 15 minutes apart. An agent who works this market daily sees patterns in the data and the deals that you cannot get from a listing website.

Since the recent changes to how buyer's agent compensation works, it is more important than ever to have a clear conversation with your agent about how they are paid before you start working together. A good agent will explain this upfront with no awkwardness.

House Hunting in Portland: What to Expect

Portland's inventory has loosened compared to the frenzy of 2021 and 2022. Homes are spending more time on the market, bidding wars are less common, and asking for inspection contingencies is standard practice again. That is good news for first-time buyers who need time to think, compare, and make confident decisions.

That said, well-priced homes in desirable areas still move. You want to be pre-approved and ready to act when the right one shows up. Tour homes with a critical eye: focus on the bones of the house, including the roof, foundation, electrical, plumbing, and HVAC. Paint colors and dated kitchens are cosmetic. A failing foundation is not.

Keep a running list of needs versus wants, and be honest about the difference. Your home buying process overview breaks this down further. If you are still narrowing down where in the metro to focus, our living in Portland guide covers the different quadrants, suburbs, and commute realities.

One thing first-time buyers often underestimate: the emotional side of the search. You will probably lose a home or two before you get one. That is normal in any market. Having an agent who keeps you grounded, recalibrates quickly, and stays proactive about finding the next option matters more than most people realize until they are in the middle of it.

From Offer to Keys: What Happens After You Find the One

Once you find a home you want, the process moves fast. Here is what to expect at each stage, and where agent expertise matters most.

Writing the Offer

Your agent will help you structure an offer that balances competitiveness with protection. This includes the price, earnest money deposit (typically 1% to 2% in the Portland metro), your proposed closing date, and your contingencies. Contingencies are your safety nets: inspection, appraisal, and financing. In today's market, keeping all three is standard practice, and you should think carefully before waiving any of them on your first purchase. How you structure the offer, including the terms, the timeline, and even the tone of any communication with the listing agent, can be the difference between getting the home and losing it. For more on this, see our guide on how to write a winning offer.

Inspections

The home inspection is one of the most important steps in the entire process. A licensed Oregon inspector will examine the structure, roof, electrical, plumbing, HVAC, and foundation. In Portland, there are also inspection considerations that are unique to this market: underground heating oil tanks from the mid-20th century, older sewer lines that may need scoping, and radon levels that vary by neighborhood. Your agent should be advising you on which specialty inspections are worth ordering based on the specific property and its location. After the inspection, your agent negotiates on your behalf, whether that means requesting repairs, asking for a credit, or in some cases, walking away. This is where experience in the Portland market pays for itself.

Appraisal and Closing

Your lender orders an independent appraisal to confirm the home's value supports the loan amount. If it comes in at or above the purchase price, you move forward. If it comes in low, your agent helps you navigate the options, which typically include renegotiating the price, covering the gap, or exercising your contingency.

Closing in Oregon typically happens at a title company or escrow office 30 to 45 days after your offer is accepted. You will sign documents, wire your remaining funds, and receive the keys. Your lender provides a Closing Disclosure at least three business days before closing that itemizes every cost. Budget 2% to 5% of the purchase price for closing costs. Oregon does not charge a state transfer tax on residential sales, which saves you money compared to many other states. Review the Closing Disclosure carefully and ask questions about anything that does not match what you expected.

Negotiating in Portland's Current Market

In a more balanced market, you have leverage. Homes sitting longer than 30 days often signal a motivated seller. Your agent can pull comparable sales data to support a below-asking offer and negotiate for seller concessions toward closing costs, which many sellers are agreeing to right now. A skilled negotiation can reduce your out-of-pocket costs by thousands of dollars. This is one of the highest-value moments in the entire process, and it is where your agent's knowledge of the local market directly impacts your bottom line.

When This Guide Does Not Apply

When This Does Not Apply

This guide is written for buyers purchasing a primary residence in the Portland metro area using traditional financing. If you are buying with cash, purchasing investment property, buying new construction directly from a builder, or purchasing land, several of these steps will differ significantly. New construction involves a different timeline, different inspection considerations, and often uses the builder's preferred lender and title company. If you are purchasing outside the Portland metro but still in Oregon, the process is similar but local programs, market conditions, and typical costs vary by county.

Why Buyers Work With Joe

- Education-first approach. Joe explains what is happening at every stage, lays out your options clearly, and lets you make the call. You will never feel pressured or left wondering what comes next.

- 10 years in the Portland metro market. He knows the neighborhoods, the pricing patterns, the inspection red flags, and the negotiation strategies that are specific to this area.

- 20+ years of sales, marketing, and leadership experience. Skilled negotiation is not something Joe is learning on your deal. It is the foundation of his career.

- You lead the decisions, Joe leads the process. From identifying the right areas for your budget to structuring an offer that protects you to navigating inspections and closing, Joe keeps things moving while you stay in control.

- Trusted vendor network. Lenders, inspectors, contractors, title professionals. Joe connects you with local vendors he has seen deliver for his clients, so you are not searching for the right people in the middle of the process.

Frequently Asked Questions About Buying a Home in Portland

How much money do I need to buy a house in Portland?

Plan for a down payment of 3% to 20% of the purchase price plus 2% to 5% for closing costs. On a $475,000 home with 5% down, that means roughly $23,750 for the down payment and $14,000 to $19,000 for closing costs. Oregon and Portland both offer assistance programs that can reduce these amounts for qualifying buyers. Your lender can calculate the specific number based on your loan type and available programs, and your agent can help you identify realistic price points where your savings work.

What credit score do I need to buy a home in Oregon?

Most conventional loan programs require a minimum of 620. FHA loans can work with scores as low as 580 with 3.5% down. Oregon's state-level assistance programs generally require a 620 minimum. A higher score gets you a better rate, which directly affects your monthly payment and what you can afford. If your score needs work, a few months of focused effort can make a significant difference.

How long does it take to buy a house in Portland?

From accepted offer to closing, typically 30 to 45 days. The overall timeline depends on how long you spend getting pre-approved and searching. Many first-time buyers spend 2 to 4 months finding the right home. Start the pre-approval process at least 60 days before you want to begin seriously touring homes so you are ready to move when you find the right one.

Do I need a real estate agent to buy a home in Portland?

You are not legally required to, but for first-time buyers it is strongly recommended. A local agent provides market knowledge you cannot get from a listing website, negotiation expertise during the offer and inspection stages, and guidance through the contract and closing process. In Oregon, buyer's agent compensation is negotiated as part of the transaction. A good agent will explain this clearly before you start working together.

What are property taxes like in Portland, Oregon?

Oregon's property tax system is based on assessed value rather than market value, thanks to Measures 5 and 50. This means your tax bill is often lower than you would expect based on the sale price. Effective rates in the Portland metro generally fall between 1.0% and 1.3% of assessed value. Your agent or title company can pull the specific tax history for any property you are considering, which is more useful than a general estimate.

Is Portland a good time to buy right now?

As of 2026, Portland's market is more balanced than it has been in years. Inventory has increased, homes are taking longer to sell, and bidding wars are less common. Buyers have more negotiating leverage than they did during 2021 and 2022, including the ability to keep contingencies and ask for seller concessions. Whether it is a good time for you depends on your financial readiness, your timeline, and your personal situation. If you are unsure, that is a great conversation to have with a local agent who can look at your specific numbers.

Should I buy or keep renting in Portland?

If you plan to stay at least 3 to 5 years and your projected mortgage payment is comparable to your rent, buying starts to make financial sense because you build equity with each payment. But buying only makes sense if you have stable income, manageable debt, and enough savings to cover upfront costs without draining your emergency fund. Our post on whether to buy now or rent longer walks through the specific questions to ask yourself.

What is the FHA loan limit in Portland for 2026?

The 2026 FHA loan limit for the Portland metro area, covering Clackamas, Columbia, Multnomah, Washington, and Yamhill counties, is $701,500 for a single-family home. The conforming loan limit for conventional loans in all Oregon counties is $832,750. Your lender can explain how these limits affect your options and which loan type gives you the best terms for your situation.

Thinking About Buying Your First Home in Portland?

The best time to start is before you think you are ready. Whether you are six months out or ready to start touring this weekend, a conversation about your goals, your budget, and the current market costs you nothing and gives you a clear next step.

Data verified: March 2026

Data Sources and References (as of March 2026):

- Oregon Housing and Community Services (OHCS): Homebuyer Programs

- U.S. Department of Housing and Urban Development (HUD): FHA Loan Limits

- Federal Housing Finance Agency (FHFA): 2026 Conforming Loan Limits

- Oregon Department of Revenue: Property Tax Information

- Consumer Financial Protection Bureau: Owning a Home

The information in this post is for general educational purposes and does not constitute financial, legal, or tax advice. Consult a qualified professional for guidance specific to your situation.

Saling Homes at eXp Realty is committed to equal housing opportunity. We do not discriminate on the basis of race, color, religion, sex, handicap, familial status, or national origin.

Categories

Recent Posts

GET MORE INFORMATION