How Much House Can I Afford in Portland?

Portland, Oregon — Working through the numbers before making an offer. What you qualify for and what you can comfortably afford are two different figures.

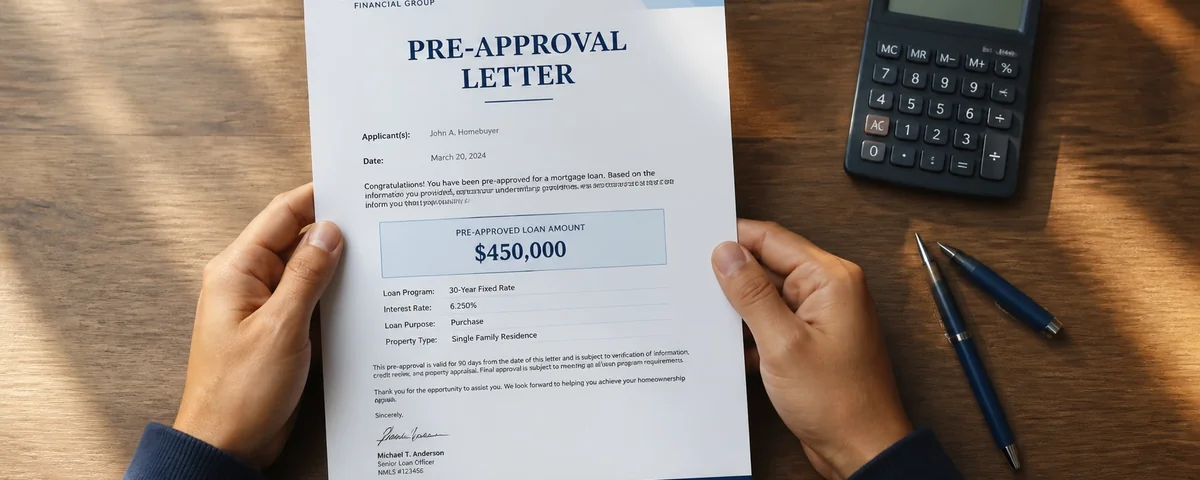

The pre-approval letter gives you a ceiling. Your actual budget is a different number — usually lower, and always more personal. How much house you can afford in Portland depends on your income, your debts, your down payment, and how much financial breathing room you want to keep after the keys are in your hand. This guide runs the real math on what Portland homes cost at today's rates, so you can walk into a conversation with a lender already knowing your range.

How Much House Can I Afford in Portland?

At current Portland-area prices and a 6.75% conventional rate, buying the median-priced home (~$516,000) with 20% down requires roughly $3,228 per month in principal, interest, taxes, and insurance — and a gross household income of approximately $108,000 to $138,000 depending on your other debts. With 3.5% down on an FHA loan, the same home runs closer to $3,981/month and requires $133,000 to $171,000 in income. Most Portland buyers find their realistic budget lands between $400,000 and $600,000 — a range where 55% of Portland metro sales closed in late 2025.

→ Bottom line: to buy a $516,000 Portland home conventionally with 20% down, plan on roughly $3,200/month and $110,000+ in household income.

The Two Numbers That Actually Matter

There are two affordability numbers every Portland buyer needs to understand before they start touring homes. The first is what a lender will approve you for. The second is what you can actually afford without stretching your finances thin. They are almost never the same number.

Lenders approve loans based on your debt-to-income ratio — a formula that compares your gross monthly income to your monthly debt obligations. The math is straightforward and doesn't account for your actual lifestyle. It doesn't know whether you have childcare costs, whether you're saving for retirement, whether you like to travel, or whether you'd feel anxious carrying a $3,800 monthly payment. Lenders approve you up to the edge of what their formula allows. Living comfortably with a mortgage is a different calculation entirely.

The purchase price is the number that gets all the attention. But the monthly payment is the number you live with every month for the next 30 years. In Portland, where homes in the same price range can sit in very different neighborhoods with very different commute times, tax rates, and HOA situations, two homes at $550,000 can have meaningfully different total monthly costs. Understanding both numbers — the purchase price ceiling and the comfortable monthly budget — is the right place to start before you ever talk to a lender.

For context on how the buying process works from pre-approval through closing, the first-time home buyer guide for Portland walks through the full sequence.

How Much House Can I Afford in Portland?

The table below shows estimated monthly payments and income requirements at five common Portland-area price points, for both conventional (20% down, 6.75%) and FHA (3.5% down, 6.5%) loans. Select the price closest to your target.

Portland Affordability Estimator — Select a Purchase Price

Assumes 6.75% conventional / 6.5% FHA, 30-year fixed, 0.97% OR property tax, $1,600/yr insurance. All data visible below for every price point.

Purchase price: $350,000 — entry-level Portland market; inner east-side condos, outer SE/NE single family

Conventional — 20% Down

$70,000 down payment

$2,232/mo

P&I $1,816 + tax $283 + ins $133

Income needed: $96K–$107K/yr

FHA — 3.5% Down

$12,250 down payment

$2,743/mo

P&I $2,172 + MIP $155 + tax $283 + ins $133

Income needed: ~$118K/yr

Income ranges use 28–36% front-end DTI. FHA figure uses 28% (more conservative). Excludes other monthly debts — student loans, car payments, and credit cards reduce your buying power further.

Purchase price: $450,000 — first-time buyer sweet spot; outer NE/SE Portland, Gresham, parts of Beaverton

Conventional — 20% Down

$90,000 down payment

$2,832/mo

P&I $2,335 + tax $364 + ins $133

Income needed: $121K–$150K/yr

FHA — 3.5% Down

$15,750 down payment

$3,489/mo

P&I $2,793 + MIP $199 + tax $364 + ins $133

Income needed: ~$150K/yr

Income ranges use 28–36% front-end DTI. FHA figure uses 28%. Excludes other monthly debts.

Purchase price: $550,000 — near Portland median; close-in SE/NE Portland, inner Beaverton, Lake Oswego entry

Conventional — 20% Down

$110,000 down payment

$3,432/mo

P&I $2,854 + tax $445 + ins $133

Income needed: $147K–$181K/yr

FHA — 3.5% Down

$19,250 down payment

$4,235/mo

P&I $3,413 + MIP $243 + tax $445 + ins $133

Income needed: ~$181K/yr

Income ranges use 28–36% front-end DTI. FHA figure uses 28%. Excludes other monthly debts.

Purchase price: $650,000 — move-up range; Sellwood, Irvington, inner Tigard, Lake Oswego mid-range

Conventional — 20% Down

$130,000 down payment

$4,031/mo

P&I $3,373 + tax $525 + ins $133

Income needed: $173K–$213K/yr

FHA — 3.5% Down

$22,750 down payment

$4,980/mo

P&I $4,034 + MIP $287 + tax $525 + ins $133

Income needed: ~$213K/yr

Income ranges use 28–36% front-end DTI. FHA figure uses 28%. Excludes other monthly debts.

Purchase price: $750,000 — upper move-up; Lake Oswego, SW Portland hills, Tigard Bull Mountain, Sherwood

Conventional — 20% Down

$150,000 down payment

$4,631/mo

P&I $3,892 + tax $606 + ins $133

Income needed: $198K–$245K/yr

FHA — 3.5% Down

$26,250 down payment

$5,726/mo

P&I $4,655 + MIP $332 + tax $606 + ins $133

Income needed: ~$245K/yr

Income ranges use 28–36% front-end DTI. FHA figure uses 28%. Excludes other monthly debts.

These are starting estimates, not quotes. Your actual payment depends on your credit score, specific lender, exact property tax rate for the county and neighborhood, and HOA dues if applicable. What these numbers do is give you a grounded reference point before you walk into a lender's office — so you know roughly what range you're working in before anyone runs your credit.

How Lenders Calculate Your Limit

Lenders use two ratios to decide how much they'll approve. The front-end ratio compares your total housing payment — principal, interest, taxes, insurance, and any HOA dues — to your gross monthly income. Most conventional lenders want this at or below 28%. The back-end ratio adds all your other monthly debt payments (student loans, car payments, credit cards, personal loans) to the housing payment and compares that total to your gross income. Conventional lenders typically want this below 43-45%, though they'll sometimes go higher with strong credit and reserves.

FHA loans allow higher ratios — sometimes up to 57% back-end with compensating factors like large cash reserves or strong credit. That sounds like more flexibility, but it's worth being careful: a lender approving you at a 55% back-end DTI means more than half your gross income is going to debt service. That's a mathematically valid approval and a financially stressful life.

Student Loans Change the Math Significantly

A buyer earning $95,000/year with $600/month in student loan payments has effectively reduced their buying power by roughly $80,000-$100,000 compared to a buyer at the same income with no student debt. Lenders count all income-based repayment amounts, even if they're currently $0 — they use a percentage of the outstanding balance if the payment is deferred. If you're on an income-driven repayment plan, confirm exactly how your lender will count that payment before you set a price target.

Rule of thumb: every $500/month in existing debt reduces your maximum home budget by roughly $65,000-$80,000 at current rates.

The Affordability Conversation Before the Offer

Combined income gives dual-income households access to a wider price range — but it's worth having an honest conversation about what happens if one income pauses temporarily. Lenders approve on two incomes; your comfort ceiling should account for one. A household earning $180,000 combined can likely qualify for $700,000+. Whether they should buy at that ceiling is a different question than whether they can.

The buyers I worry about are the ones who buy at the top of their approval. Not because they can't make the payment — they can, on paper. It's the months when the water heater fails and the car needs brakes and the property tax bill arrives that stretch becomes stress. I'd rather help someone buy at 85% of their approval and sleep well than max out their approval and spend the next two years anxious.

Field note

For a detailed walkthrough of how to choose the right agent to help you navigate this process, see how to choose a real estate agent in Portland.

Already know your budget? The next question is what you'll owe at closing on top of the down payment. See what closing costs in Oregon actually look like →

Down Payment Options in Oregon

Oregon buyers have more down payment options than most realize. The right choice depends on how much cash you have, how much you want to preserve as a reserve, and whether you'd rather have a lower monthly payment or more liquidity after closing.

| Down Payment | Loan Type | On $450K | On $550K | PMI / MIP? | Notes |

|---|---|---|---|---|---|

| 3% | Conventional (HomeReady/Home Possible) | $13,500 | $16,500 | Yes — PMI until 20% equity | First-time buyers; income limits apply |

| 3.5% | FHA | $15,750 | $19,250 | Yes — MIP for life of loan (if <10% down) | Lower credit score OK; upfront MIP 1.75% |

| 5% | Conventional | $22,500 | $27,500 | Yes — PMI until 20% equity | Most common non-FHA low-down option |

| 10% | Conventional | $45,000 | $55,000 | Yes — PMI until 20% equity; lower rate than 5% | Lower monthly PMI premium than 5% down |

| 20% | Conventional | $90,000 | $110,000 | No | No PMI; lowest monthly payment; strongest offer |

| 0% | VA (eligible veterans) | $0 | $0 | No MIP; funding fee instead (can be financed) | VA-eligible buyers only; strong competitive advantage |

Oregon Bond Loan (OHCS): Oregon Housing and Community Services offers the Oregon Bond Residential Loan Program, which provides below-market interest rates to first-time buyers and those who haven't owned a home in the past three years. Income and purchase price limits apply and vary by county. It can be combined with the Oregon Bond Down Payment Assistance loan, which provides 3-4% of the loan amount as a second loan for down payment and closing costs. This program is worth asking your lender about specifically — not every lender participates, and eligibility is more flexible than many buyers assume.

The down payment decision involves tradeoffs that depend on your specific situation. Putting more down reduces your monthly payment and eliminates PMI sooner, but leaves you with less cash reserve after closing. Putting less down preserves cash but increases your monthly payment and total interest paid. There's no universally correct answer. For a full picture of what your cash-to-close requirement looks like beyond the down payment, see the closing costs in Oregon guide.

What $400K–$650K Buys in Portland Right Now

Numbers are more useful when they connect to actual properties. Here's what different price points have been delivering in the Portland metro market as of early 2026, based on RMLS activity:

$350,000–$425,000: Entry-level single-family homes in outer Southeast or outer Northeast Portland, Lents, Montavilla, and Centennial. Smaller square footage (under 1,400 sq ft), older homes (1940s-1960s) that may need updating. Also covers condos in inner neighborhoods — Pearl District studios, Lloyd District one-bedrooms. This range consistently sees multiple offers on move-in-ready properties.

$425,000–$575,000: The most active price band in the Portland metro — 55% of Portland metro sales closed in the $300,000-$600,000 range in late 2025. This buys 3-bedroom Craftsman or foursquare homes in inner SE and NE Portland, updated ranches in Beaverton and Hillsboro, and newer construction townhomes in outer neighborhoods. Move-in-ready homes in this range are competitive. Homes needing work are sitting longer and offering more negotiating room.

$575,000–$700,000: Move-up range. Larger homes (1,800-2,400 sq ft) in Sellwood-Moreland, Irvington, Eastmoreland, inner Tigard, and Lake Oswego entry-level. You're more likely to find original character, larger lots, and proximity to close-in amenities. This range is more balanced currently — less competition, more room to negotiate on price and terms.

The real advantage of understanding your number before you shop is that you can match budget to neighborhood realistically before you fall in love with a specific home. A buyer who knows their comfortable ceiling is $520,000 can target Sellwood for a smaller house or pivot to Lents for a larger one — but only if they've done the math first. For help connecting your budget to specific Portland neighborhoods, the total cost of homeownership beyond the payment post covers what ongoing costs look like once you're in.

Oregon's new construction pipeline is also adding supply at the $450,000-$650,000 range as HB 4037 implementation moves forward — worth knowing if you're open to new builds as part of your search.

When These Estimates Don't Apply

Five Situations Where the Standard Formula Breaks Down

Self-employed buyers: Lenders use two years of tax returns for self-employed income, which often shows less income than the business actually generates due to legitimate deductions. Your qualifying income may be significantly lower than your actual cash flow. A lender who specializes in self-employed borrowers will underwrite differently than a standard retail bank.

Commission or variable income: Lenders typically average two years of variable income. If your income increased significantly last year, the average pulls your qualifying number lower than your current earnings. Timing of loan application relative to tax year matters.

HOA properties: Condos and planned communities with HOA dues add directly to your front-end DTI. A $400/month HOA on a $500,000 condo reduces your effective buying power by roughly $50,000-$60,000 compared to the same purchase price without an HOA.

Properties with ADUs or rental income: Some lenders will credit a portion of existing rental income toward your qualifying income, which can increase buying power. Rules vary by loan type and lender. Worth asking about specifically if the property has an income-producing unit.

Rate changes: The estimates here use 6.75% conventional and 6.5% FHA. A 0.5% rate change shifts the monthly payment on a $440,000 loan by roughly $140/month — which translates to about $20,000-$25,000 in buying power. Get a fresh Loan Estimate from a lender for current rate quotes before finalizing your budget.

Frequently Asked Questions About Portland Home Affordability

How much house can I afford in Portland?

At current rates (6.75% conventional, 6.5% FHA) and Portland's median price around $516,000, buying with 20% down requires roughly $3,228/month in PITI and household income of approximately $108,000 to $138,000 depending on other debts. With FHA at 3.5% down, the same home runs about $3,981/month and requires $133,000 to $171,000 in income. Most Portland buyers find their realistic range lands between $400,000 and $600,000 — the price band where 55% of metro sales closed in late 2025. The affordability calculator above shows payment and income estimates for five common price points. A lender pre-approval will give you a personalized ceiling based on your actual income, debts, and credit score.

What income do I need to buy a house in Portland?

To buy at Portland's median price of approximately $516,000 with 20% down at 6.75%, you need roughly $108,000 to $138,000 in gross household income assuming no other major debts. With student loans, a car payment, or other monthly obligations, that number rises. FHA buyers at 3.5% down on the same home need approximately $133,000 to $171,000. Oregon's median household income is around $78,000 — which illustrates why the Portland market is challenging for single-income buyers at the median price, and why dual-income households and buyers with significant down payment savings have a meaningful advantage.

What is the minimum down payment to buy a home in Oregon?

Oregon buyers can purchase with as little as 3% down on a conventional loan (through Fannie Mae HomeReady or Freddie Mac Home Possible programs, which have income limits) or 3.5% down on an FHA loan. VA-eligible buyers can purchase with 0% down. USDA loans also offer zero down for properties in eligible rural areas — some outer Portland suburbs qualify. Oregon Housing and Community Services also offers the Oregon Bond Loan program with below-market rates and down payment assistance for eligible first-time buyers. Income and purchase price limits apply. Not every lender participates in all programs, so it's worth asking specifically when you shop lenders.

How does debt-to-income ratio affect what I can afford in Portland?

Your debt-to-income ratio is one of the primary factors lenders use to set your approval ceiling. The front-end ratio (housing costs only) should ideally stay at or below 28% of gross monthly income for conventional loans. The back-end ratio (housing plus all other monthly debts) should stay at or below 43-45% for conventional, though FHA allows higher with compensating factors. Every $500/month in existing debt — student loans, car payments, credit card minimums — reduces your buying power by roughly $65,000-$80,000 at current rates. If you're close to your limits, paying down installment debt before applying can meaningfully increase your qualified amount.

Is Portland affordable for first-time buyers in 2026?

It's more accessible than it was at peak 2022 competition, but still challenging at the median price. The Portland metro has had over 110 consecutive days with conventional rates below 6.5%, which has improved buying power compared to 2023-2024. Price growth has flattened — the Zillow Home Values Index showed a slight year-over-year dip as of early 2026. The $400,000-$550,000 range remains the most active and competitive. First-time buyers with pre-approvals in hand, flexibility on neighborhood, and realistic price targets are finding success. The biggest barriers remain the down payment accumulation and competition from move-up buyers who carry equity from prior sales.

Does Oregon have any down payment assistance programs?

Yes. The Oregon Bond Residential Loan Program through Oregon Housing and Community Services (OHCS) provides below-market interest rates for eligible first-time buyers and repeat buyers who haven't owned in the past three years. It can be paired with the Oregon Bond Down Payment Assistance loan, which offers 3-4% of the loan amount as a second loan to help cover down payment and closing costs. Income limits and purchase price limits apply and vary by county. Some Oregon cities and counties also have local assistance programs. These programs are worth asking your lender about specifically — eligibility is broader than many buyers assume, and not every lender participates. See the OHCS Oregon Bond program page for current limits.

Should I buy at the top of my budget in Portland?

Generally, no. Buying at the top of your lender-approved limit means your monthly payment takes up the maximum share of income your lender will allow — leaving little margin for the normal costs of homeownership like maintenance, repairs, and property tax increases. A better approach is to identify your comfortable monthly payment first, then work backward to a purchase price. Buying at 85-90% of your approval ceiling typically gives you enough room to absorb routine costs without financial stress. If you're torn between a home that's right at your limit and one that's comfortably within it, the one within your budget will almost always feel better to live in two years after closing.

What Does Your Number Actually Look Like?

The estimates here give you a starting point. Your actual budget depends on your credit score, your debts, the specific lender you work with, and which neighborhoods you're targeting. I walk every buyer through this math before we ever look at a single property — so your price range is grounded in reality before you start falling in love with homes. If you want to talk through what your range looks like in today's Portland market, let's do that.

Portland Metro Homes for Sale

Browse current listings across the Portland metro area.

- CFPB — What is a debt-to-income ratio?

- Oregon Housing and Community Services — Oregon Bond Residential Loan Program

- Oregon Department of Revenue — Property Tax Statistics

- Fannie Mae — HomeReady Mortgage (3% down program guidelines)

- HUD — FHA Loan Information (3.5% down, DTI guidelines)

- Federal Reserve Bank of St. Louis (FRED) — 30-Year Fixed Mortgage Rate

- Bureau of Labor Statistics — Oregon Economy at a Glance

- Insurance.com — Average Homeowners Insurance by State, 2025

Data verified: May 2026. Mortgage payment estimates use May 2026 rate environment. Consult a licensed lender for current rate quotes.

The information in this post is for general educational purposes and does not constitute financial, legal, or tax advice. Mortgage payment estimates are illustrative and based on stated assumptions — actual payments will vary based on your credit score, lender, exact rate, property tax rate, and insurance premium. Consult a qualified mortgage professional for guidance specific to your situation.

Saling Homes at eXp Realty is committed to equal housing opportunity. We do not discriminate on the basis of race, color, religion, sex, handicap, familial status, or national origin.

Categories

- All Blogs (90)

- Buying a Home (33)

- Community Page (14)

- Downsizing (7)

- Home Buying Process (7)

- Homeownership (6)

- Increasing Your Homes Value (4)

- Local Events (2)

- Market Update (18)

- Mortgage Information (9)

- Neighborhood Eats and Experiences (1)

- neighborhood info (3)

- Real Estate News (12)

- Selling Your Home (18)

Recent Posts

GET MORE INFORMATION